Ohio Sales Tax Holiday

From August 1st, 2025 through August 14th, 2025, you can shop tax-free. We are offering NO TAX on any individual part(s) for your vehicle that are $500 and under.

Any individual parts $500 in over, standard tax will apply. Must be paid for and received before August 14th to apply for tax-free holiday.

While we're excited for all Ohioans to take advantage of the upcoming Sales Tax Holiday from August 1st, 2025 to August 14th, 2025, we want to clarify how it applies to you.

Read more here:

- When is the sales tax holiday? Ohio's sales tax holiday is from 12:00 a.m. Friday, August 1 until 11:59 p.m. Thursday, August 14, 2025.

- What items qualify for the sales tax holiday? The sales tax holiday will include all tangible personal property that is $500 or less.

- Can a dealership choose not to participate in the sales tax holiday? No. The sales tax holiday is set by law and dealerships must comply.

- Does the exemption apply to rebates? Rebates occur after the sale and do not reduce the sales price of an item for purposes of the sales tax holiday threshold. If the price of the item before rebate exceeds the threshold, it is taxable.

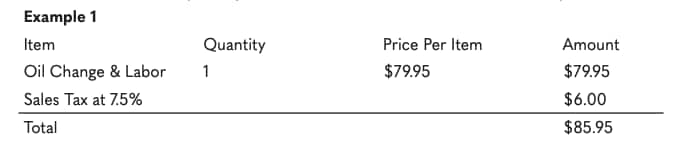

- Oil Changes and Shop Supply Charges. If there is one flat price for an oil change, and labor isn't itemized separately from the tangible personal property (e.g., parts, oil, oil filter, etc.), then the entire transaction is subject to tax and does not qualify for the holiday. If there is an itemization on the invoice that separates the tangible personal property from the labor, and all tangible personal property individually are all below $500, the labor qualifies for the tax holiday and is tax exempt along with the tangible personal property.

- What items do NOT qualify for the sales tax holiday? The sales tax holiday will not apply to tangible personal property that is over $500 and services with some important exceptions. (see FAQ 6 for more on services). Watercraft or outboard motors required to be titled pursuant to Chapter 1548 of the Revised Code, motor vehicles, are also not included in the sales tax holiday. Tangible personal property that is sold in connection with the sale of a motor vehicle is also not included. For example, if a customer purchases a motor vehicle and running boards at $135 each in the same transaction, the running boards would considered part of the sale of the vehicle and would not be exempt from sales tax. However, if a customer purchases a motor vehicle and completes the transaction and then walks into your Parts Department immediately afterwards to purchase the running boards, the running boards would be tax exempt.

- Can multiple qualifying items be purchased in a single tax-exempt transaction? Yes. There is no limit on the amount of the total purchase. The qualification is determined item by item. For example, the purchase of four tires (each tire costing $250, total purchase $1,000) would all be tax exempt.

- When does a repair have to occur for the holiday to apply? For the sales tax holiday exemption to apply, all aspects of the repair must occur during the holiday period. Specifically, the repair order must be opened, the parts or other items must be ordered, the repair completed, and the repair paid for within the holiday period. Additionally, if parts are ordered for shipment, they must be ordered, paid for, and shipped - all within the holiday period.To clarify, repairs initiated on or before July 31, 2025, but completed during the tax holiday, do not qualify for the exemption. Similarly, repairs that occur during the tax holiday but are not completed and paid for until after the holiday ends are not eligible for the exemption. Additionally, even if a repair is partially completed during the holiday, it does not qualify for the exemption if it is finalized after the holiday period.

- Does the exemption apply to services? Generally, the exemption does not apply to taxable services, However, different rules apply if the service is the repair or installation of tangible personal property.

- If items that meet the exemption ($500 or less) are sold in connection with services that do not meet the exemption for one non-itemized price, then the entire price is subject to sales tax.

- If the price of the exempt items and taxable services are separately stated, then the sales tax exemption can be applied to the exempt items.

- If the service is the repair or installation of tangible personal property, like service or repair of a motor vehicle, the service itself can also be exempt if the tangible personal property installed or the value of the repair parts are $500 or less. For the holiday exemption to apply, the parts and the service must be separately stated on the invoice.

Below are some examples:

In this example, since there is no separation of the price for the service, the entire price does not qualify for the holiday.

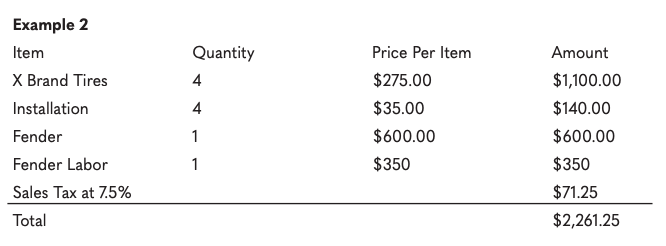

In this example, each tire is below the $500 threshold and would be exempt under the holiday. Also, since the tires qualify, and installation labor for those tires is separately stated, the labor would also be exempt under the holiday.

However, although the fender installation labor is also separately stated, because the price of the fender is over the $500 threshold and does NOT qualify for the holiday, both the fender and the labor to install do not qualify for the holiday.

Please note in the example above that the installation/labor cost will be exempt from sales tax if the price of the part (tangible personal property) is $500 or less, even if the installation/labor cost exceeds $500.

Information cited from: 2025 Sales Tax Holiday FAQs - Motor Vehicles